$GFG.DE - Global Fashion Group

Struggling fashion e-commerce marketplace trades at ~30% of net cash with opportunities to salvage equity value

Special thanks and credit to SchopenhauerCap for flagging this idea and covering it over the last several years on Twitter (with many ideas/thoughts outlined below belonging to him). Not investment advice. DYODD. Uncertainty is the only certainty. Yes - the business may in fact end up being a zero.

Key Stats

Price: €0.30

Shares Out: 222M

Market Cap: €65M (€206M net cash at end of '23)

EV: ~(€140M)

2022 sales: €1.1B / 2023E sales: €800M

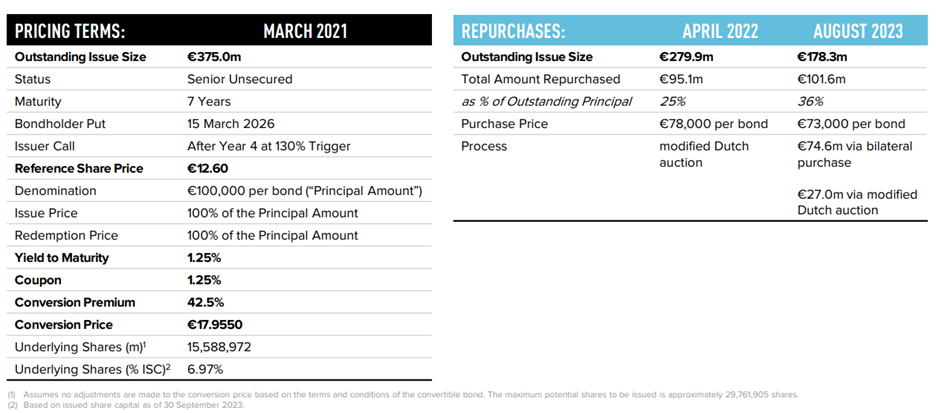

Notable LT Liabilities: €178M 2028 convertible bonds outstanding at 1.25% coupon & €17.95 share price convert (valued at par in EV) Investment Thesis

Shares of Global Fashion Group, an online fashion retailer/marketplace, have sold off significantly in recent years after reaching lofty heights during the pandemic. Once viewed as the future ‘Zalando of emerging markets’ - the company is now viewed by the market as a collection of terminally profitless negative value companies. But after building cash and reacquiring discounted debt in Q4’23, GFG ends the year trading at a steep discount to net cash. And opportunity may exist to stem the bleeding in its operating performance and salvage equity value. GFG (really 3 separate geography-focused businesses) is not a GoodCo by any means (one may go so far as to call it a BadCo… or worse). But the operating businesses should have at least SOME (however small) salvageable value and the current steep discount to cash on hand gives us a margin of safety as management attempts to turn things around. The overall thesis revolves around these points:

[Key point] After a punishing several years, GFG currently trades at a deeply discounted market cap of €65M (down ~98%+ from it’s COVID highs) but ends 2023 with €206M net cash - so is trading at a deeply negative EV and just ~30% of net cash

While the business’ current outlook is certainly not enviable, GFG is taking steps to stem the bleeding by cutting costs and phasing out its worst performing operations

Management has behaved rationally in the past (e.g., issuing low cost convertible debt in March ‘21 at very favorable terms, since then buying back over half of this debt at 30% discount to par, successfully selling off it’s Russian operation Lamoda in late ‘22 following the start of the Ukraine war for ~€100M) and I expect them to continue to do so to try to turnaround the business & create whatever value is possible for shareholders

The company has stated they’re considering all options including cutting costs, ceasing underperforming operations, and potentially divesting underperforming brands. Successful near term execution on any key value creating lever could meaningfully re-rate the stock (which has already run up ~30-50% after the company pre-reported slightly better than anticipated q4’24 results)

Even if they’re not worth much, GFG’s three remaining individual brands may have some value to a strategic buyer in select markets

Lastly, the company is majority owned by two major institutional investors (Kinnevik & Rocket Internet) who I believe should be aligned on salvaging as much value as possible for the shareholders

Company Overview & History - How we got to where we are

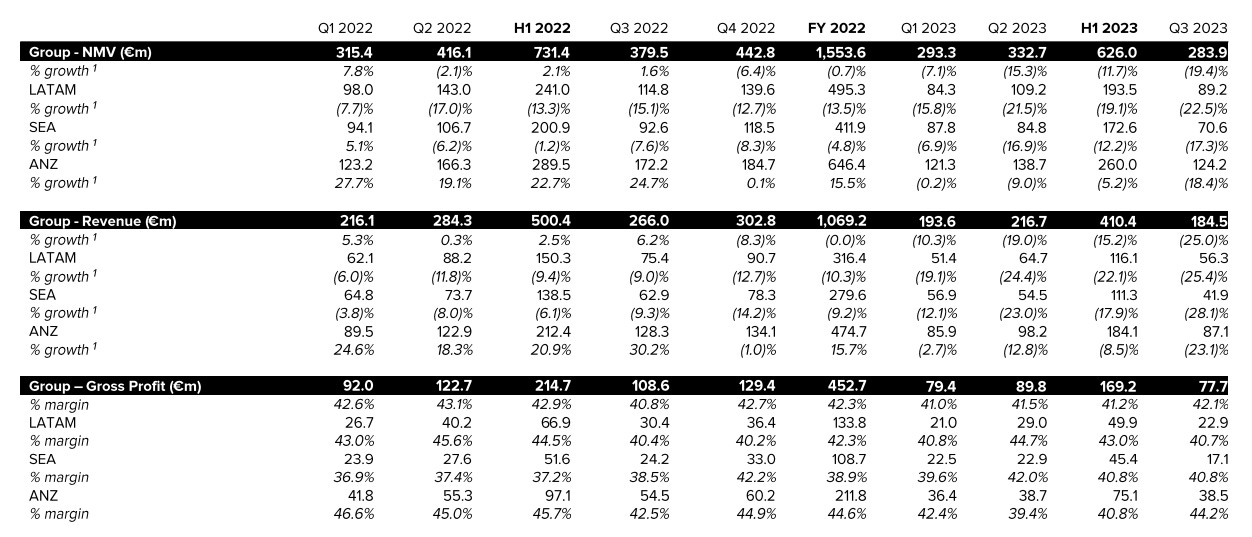

Global Fashion Group is an operator of e-commerce retail and marketplace platforms with current operations in 3 key regions1: Australia / New Zealand (The Iconic brand), LatAm2 (dafiti), and Southeast Asia3 (Zalora). The company is majority owned by Kinnevik (37%) and Rocket Internet (24% combined between two holding entities) who’ve been involved in the company since founding it as a joint venture in 2011. GFG helps its fashion brand partners access smaller or emerging markets by selling their products through a traditional retail model (where GFG assumes inventory) as well as a marketplace model where brand partners directly list products on GFG’s apps/websites (and may also rely on them for a mix of warehousing/delivery services). The company currently has ~9M active customers across markets, will do ~€1.3B NMV of sales in 2023 and ~€800M revenue (down ~14% and 25% respectively).

Despite never being profitable, the business has traded at nosebleed valuations multiple times before. Both on the private markets (e.g., in 2016 Kinnevik had to cut its private mark from €1.6B to €1.0B) as well as on the public market (after going public in 2019, the stock traded as high as €14/share or ~€3B market cap during peak 2021 tech-mania) - as revenue/NMV continued to show solid topline growth of 10-20%+ and investors hoped the company could realize similar success to Zalando (another Rocket Internet seeded company). The company’s ongoing shift from a direct retailer to a marketplace (no inventory) model was believed to be a significant long term tailwind to margins. And management and investors repeatedly pitched the company’s unique value proposition for brands, giving them easy access to diverse and challenging-to-operate-in small/emerging markets and a bundle of GTM options (wholesaling into a retail channel or retaining inventory and relying on GFG for a mix of marketing, warehousing, and delivery support services).

However, the last few years have been punishing and the bull thesis has obviously not played out. Topline revenue (of current operations) peaked in 2021, declining slowly into ‘22 then rapidly in ‘23 as the company faced tougher comps and heightened competition (especially in SEA & LatAm). In 2022, Russia invaded Ukraine and GFG ended up having to sell off it’s Russian business unit Lamoda, arguably the gem of its portfolio, for just ~€100M to a Russian department store owner. While this price doesn’t seem too bad (especially in the context of the company’s current valuation), Lamoda was the largest, fastest growing, and only consistently EBITDA positive business unit for GFG (more on this later and what it might mean for the current business valuation) - the Lamoda business was ultimately sold off for just ~3x segment adj. ‘21 EBITDA, after growing it’s topline ~20% in ‘21 and with ~30-40% growth momentum going into ‘22.

Candidly, the valuation for most of the company’s history didn’t make sense and would never have been justified regardless of operating performance. So it’s not surprising the stock is down big. But to say the last couple years have been a disaster would be an understatement. Growth stalled into ‘22 then utterly collapsed in ‘23. No business unit has been spared - with teens % declines in NMV and 20-30% revenue declines across the board (NMV declining slower than revenue as marketplace share of NMV vs. traditional retail continues to rise). The LatAm business unit Dafiti has been a particular disaster (even before ‘22 the LatAm business was underperforming, barely growing into ‘21 as sales elsewhere ripped higher) and moneypit. But perhaps most worrying, the ANZ business The Iconic, the most valuable remaining asset GFG possesses (with ~40% of group revenue) has seen sales and profitability fall rapidly as well.

All in all, the growth story is dead. The stock is down 98%. The question now is can the business retrench, cut costs, stabilize what can be saved, and sell-off/exit what cannot. This is obviously a large cultural shift for a VC / growth investor backed company - and it doesn’t surprise me they’ve been slow to make the necessary cuts as the stock has been relentlessly hammered lower.

But change appears to be coming. Management has been reducing headcount and cutting costs through ‘23, which should start to show most prominently in ‘24 results. While margins deteriorated through the first three quarters of ‘23, preliminary reporting for q4’23 notes hitting EBITDA breakeven despite what will be an ~30% revenue decline for the quarter. With easier comps into ‘24, further cost cutting, and potential value creating restructuring - it just might be possible GFG gets turned around. And with plenty of cash on hand to easily weather another bad year or two of cash burn and a negative €140M EV giving us a decent margin of safety, the business could be worth a look at the current price.

See below for recent quarterly financials and performance by segment for ‘22-q3’23

Stemming the bleeding

Lastly, on overhead and capital investments, we continue to take action that will deliver a return to operating cost deleverage as demand recovers. Our Q3 total headcount and tech and admin costs both reduced close to 20% year-over-year. Despite the competing effects of inflation and lower volumes to our bottom line, our completed cost saving actions, and those still underway, will position us for a strong 2024.

- Helen Hickman, GFG CFO, q3’23 earnings call

One of shareholders’ biggest frustrations to date would be how slow GFG has been in cutting costs and the fact that they haven’t yet communicated the finer details of their strategy to cut costs to breakeven. For this investment to really work, management needs to be cutting hard and fast - which is likely a large cultural shift for a business that had been in growth mindset up until hitting a wall in 2022. But cuts have been occurring with more on their way, and the benefits of what’s been done so far should become more clear in q4’23 results as well as early ‘24 results.

In its preliminary 2024 results, management noted being adj. EBITDA ~breakeven for q4’24, which is actually on par or better than q4’22 (-1.3% adj. EBITDA margin) despite what will be an ~30% decline in revenue for the quarter YoY (assuming ~200M revenue in q4’24). Obviously the results for the first three quarters of ‘23 were far worse on a relative basis, but it would appear the company is moving in the right direction to manage profitability even as sales fall as a result of tough comps and drawn back marketing spend.

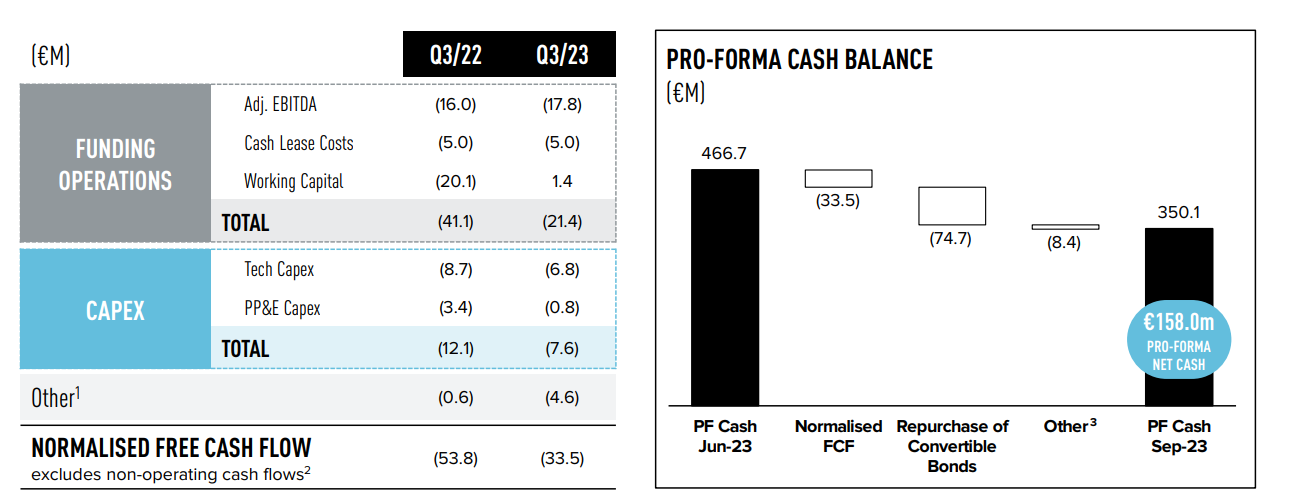

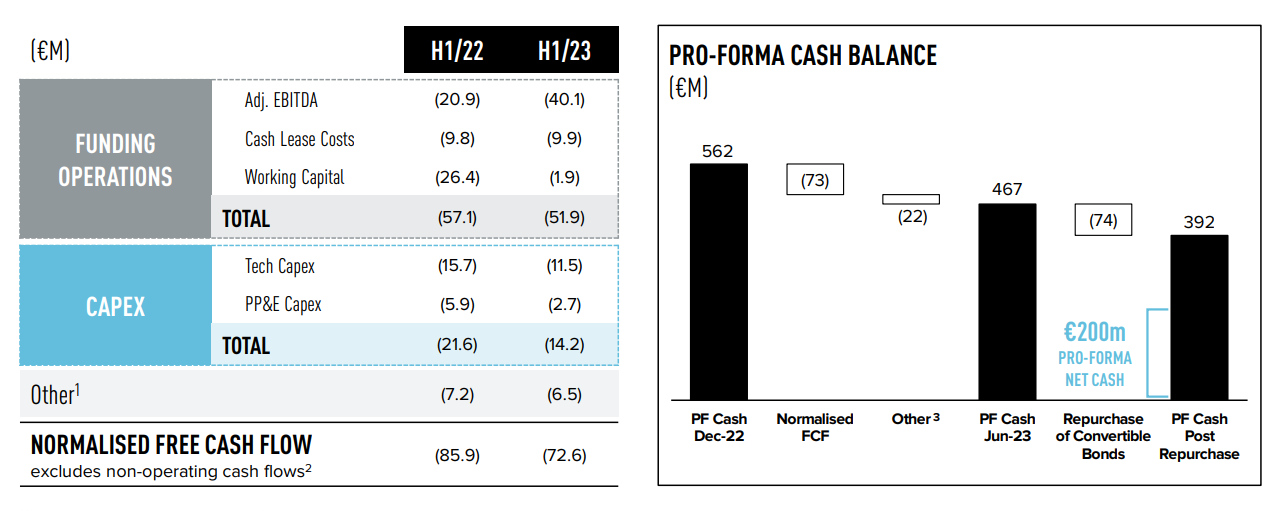

The company also built cash into year end (q4 is obviously it’s best quarter given holiday shopping), ending the year with €397M cash and €206M net cash, up from €350M/€158M respectively end of q3. This again compares favorably to prior years despite far lower revenue, and overall cash management for 2023 as a whole is actually looking better than 2022.

Overall - the company is still losing money quickly. They’ve burned through ~€90-100M in each of ‘22 and ‘23 (excluding repurchases of convertible debt and proceeds from divestments). But recent momentum suggests 2024 will look better. Even if the company burns through another ~€60-80M in ‘24 (and I believe they can do better than that), it still would end 2024 with €120-140M of net cash, or double the current market cap. So management has time to turn things around. And if results surprise to the upside, the stock should meaningfully re-rate reflecting the option value of the underlying businesses and future potential value creation levers (divestments, additional convert repurchases, etc.).

See below for cash flow from q3/q2 2023 and 2022 investor presentations

Business unit thoughts

Don’t want to drum up too much optimism here, but clearly I believe there’s opportunity to realize value / salvage the equity for existing shareholders by divesting or exiting lagging business units. The LatAm dafiti business in particular has been an absolute dog, and shutting it down or giving it away is probably in the best interest of the business at this point. GFG has already shut down Argentinian operations, and I’d hope they continue to consider exiting countries or scaling back operations wherever it doesn’t make sense.

And again, don’t want to encourage false hope - but these are businesses that strategic buyers have been rumored to have looked at in the past. For example, Brazilian department store Lojas Renner was rumored to have been looking at Dafiti back in 2021. At the time, businesses like dafiti were going for nosebleed valuations. But in a world where giving away the business for just €1 would probably be good for shareholders, being able to sell for what would have been a trivial amount a few years back could still be huge.

Then of course, consider that the company was able to sell Lamodo, the Russian business unit in late ‘22 for €100M Euros (~3x segment level adjusted EBITDA). While this was the gem of the GFG portfolio (actually profitable, higher growth) and a year earlier could have been worth multiples of that, it was still sold in a very challenging environment. Now imagine what that implies for the value of the remaining businesses assuming any of them could be stabilized. The ANZ business The Iconic (what I’d consider the remaining core asset for GFG) is an established platform in developed/stable economies, was approaching profitability before this past year, and has over €300M revenue. Could it be worth more than 0?

To be clear, I don’t know if a sale is likely or possible. Odds are probably low. And when management was asked about divesting the LatAm business on the q2 earnigns call, they threw a bit of cold water on the idea (although did note they were open to consider it).

Q: Would you consider exploring strategic options for the LatAm business?

Thanks for the question. I mean, we're definitely very focused on executing our strategy and turning the financial performance more positive through the actions on cost and also recovering the top line that we've talked about in this call and also previously. When it comes to strategic options, for any part of our business, in the end, we're rational actors and open to think about things. But we don't think this is necessarily an environment where that really lends itself to those types of activities. So we're very focused on delivering the financial objectives that we set ourselves within the financial conditions that we have and the capital we have access to.

- Christoph Barchewitz, GFG CEO, , q2’23 earnings call

Divestment or not, the point still stands that the market is assigning meaningful negative value to all of GFG’s businesses. This might in fact be right given current cash burn, but if any of the 3 businesses are worth even scraps of what they were formerly valued at, the upside for equity holders from here could be massive.

Notes on convertible debt

One other notable point here is that basically all the current public equity value of the business can be tied to management taking advantage of the free money cannon for tech/e-commerce companies back in 2021. Back when the stock price was flying high in peak COVID mania, the company initially issued €375M of convertible debt (1.25% coupon) in March 2021 at a strike price of 17.95. Obviously you can look at the current stock price and safely assume they’re probably not coming close to that strike anytime soon. Anyway, the company has bought back nearly €200M since at ~75% of par value (so that €50M cash discount is basically all the current equity value). And the remaining €178M convert liability held on the balance sheet at par is now really only worth ~€130-140M. Management has also indicated on the q3 earnings call that there may be further opportunities for EV shrinking / net-cash increasing convert repurchases. So cheers to management’s capital allocation wizardry to date that’s perhaps the only reason this is a potentially interesting opportunity at all.

We continue to look for further opportunities to further reduce our outstanding convertible bond liability, whilst balancing our cash needs.

- Helen Hickman, GFG CFO, , q3’23 earnings call

Risks - a lot

Please note: this investment is not without significant risk. The company is burning cash and there is no guarantee management will be able to turn things around. The topline is shrinking and its unclear at what point the business could be stabilized while cutting costs. The ability to sell-off or exit challenged business units (notably the LatAm dafiti business) could prove futile. Core brands face meaningful competition, especially in LatAm and SEA. And previously stronger performing business lines (The Iconic in Aus/NZ) have also seen margin deterioration (although I hope this is temporary / reverses in 2024). DYODD and do not invest money you can’t afford to lose. This is a classic deep value / turnaround situation that I’m writing up as I found it interesting. But realize there are no guarantees here. Welcome all thoughts/feedback.

GFG exited operations of Lamoda, its brand operating in Russia, Belarus & Kazakhstan in 2022 after the start of the Ukraine war, selling off that business line to Yakov Panchenko (owner of the stores of Stockmann AG, which operates department stores in Russia)

LatAm countries of operations include Brazil, Argentina, Chile & Colombia

South East Asian operations include Hong Kong, Indonesia, Malaysia, Singapore, Brunei, Taiwan, and the Philippines. Zalora Philippines is owned 51% by GFG while all other brands are 100% owned by GFG.